Introduction

The Asia-Pacific (APAC) Additive Manufacturing (AM) Market—commonly known as the 3D printing market—is experiencing rapid transformation. What once existed primarily as a prototyping technology has now evolved into a mainstream production method across several industries including aerospace, automotive, medical devices, consumer goods, heavy manufacturing, and electronics. The region benefits from a robust manufacturing environment, strong government support for industrial digitalization, and a rapidly expanding community of enterprises adopting AM for both innovation and efficiency.

As APAC countries increasingly focus on advanced manufacturing, supply chain resiliency, and localized production, additive manufacturing has become a strategic capability. The market is projected to continue growing at a high double-digit CAGR over the next decade as industries shift from prototyping toward end-use parts, tooling, spare-part digitization, and mass customization.

Source - https://www.databridgemarketresearch.com/reports/asia-pacific-additive-manufacturing-market

Market Size Overview

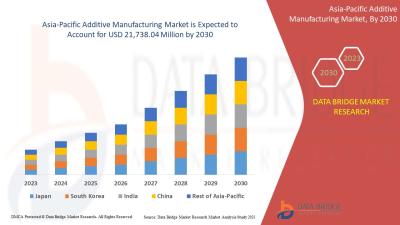

Various industry assessments of the APAC AM market place its value between USD 5–7 billion in 2023, depending on methodology (hardware-only vs. full ecosystem with materials and services). Most analyses expect the market to grow at a 20% to 27% CAGR through 2030.

This rapid expansion stems from increasing industrial adoption of metal AM, advances in polymer printing technologies, growth in dental and medical applications, and expansion of low-cost consumer and prosumer 3D printers across APAC. By 2030, the region is expected to account for a major share of global AM revenues, supported by its manufacturing strengths and large-scale industrialization.

Key Market Drivers

1. Massive Manufacturing Ecosystem

The APAC region includes the world’s largest manufacturing hubs—China, Japan, South Korea, India, and Southeast Asia. Additive manufacturing fits naturally into these environments by shortening lead times, enabling complex part designs, supporting lightweighting strategies, and reducing tooling needs. Manufacturers integrate AM into both prototyping and production workflows to boost speed and flexibility.

2. Strong Government Support

Governments across APAC are investing in advanced manufacturing programs, providing funding for R&D centers, industry–academia collaboration, and infrastructure for digital manufacturing. Several nations have national roadmaps specifically supporting additive manufacturing.

3. Healthcare and Dental Growth

Medical and dental applications are among the fastest-growing AM segments in APAC. This includes custom implants, surgical guides, dental prosthetics, orthopedics, and patient-specific anatomical models. Rapid population growth, aging demographics, and rising healthcare spending further support adoption.

4. Automotive and Mobility Transformation

The shift toward electric vehicles (EVs), autonomy, and lightweighting has encouraged automotive manufacturers to use AM for functional prototyping, jigs and fixtures, and increasingly for low-volume end-use parts. AM supports faster design cycles among automotive OEMs and component suppliers.

5. Proliferation of Affordable Desktop Printers

APAC—particularly China—has become the world center for low-cost and prosumer 3D printers. This has democratized access and accelerated adoption among small businesses, design firms, educational institutions, and hobbyists. The availability of cost-effective machines builds a broader foundation for long-term industrial AM growth.

Market Segmentation

By Technology

Powder Bed Fusion (PBF): Dominant in high-strength metal and polymer parts, widely used in aerospace, medical, and automotive.

Directed Energy Deposition (DED): Preferred for large metal components and repair applications.

Binder Jetting: Growing in demand due to higher throughput and lower part costs, ideal for metals, ceramics, and sand molds.

SLA/DLP: Popular for medical, dental, jewelry, and high-precision resin applications.

FDM/FFF: Leading in the consumer and entry-level segment, widely used for prototyping and tooling.

By Offering

Hardware: Industrial metal printers, polymer printers, desktop devices.

Materials: Metal powders, thermoplastics, photopolymers, composites, ceramics.

Software: Design tools, process simulation, build preparation, quality monitoring.

Services: Contract printing, scanning, design optimization, post-processing.

By Application

Aerospace & defense

Medical & dental

Automotive & transportation

Industrial manufacturing tools

Consumer products

Electronics

Education & research

Country-Level Insights

China

China is the largest APAC market, driven by national industrial development policies, a massive manufacturing base, and strong domestic 3D printer suppliers. Both metal and polymer AM are scaling, making China one of the fastest-growing regions globally.

Japan

Japan focuses on precision engineering and advanced materials, applying AM heavily in aerospace, electronics, and high-end manufacturing. Japanese companies prioritize reliability, certification, and integration with traditional processes.

South Korea

South Korea uses AM in automotive, electronics, medical devices, and defense. It has strong investment in next-generation materials and large-format metal AM systems.

India

India’s AM adoption is accelerating, driven by aerospace, healthcare, and educational institutions. The government promotes AM for localized production, defense, and tooling.

Australia & New Zealand

These markets focus on medical devices, research-driven innovation, mining, and defense applications. Australia is noted for strong metal AM R&D initiatives.

Competitive Landscape

The APAC market features both global leaders and strong regional players:

Global companies: Renishaw, EOS, Stratasys, 3D Systems, HP, GE Additive.

APAC-based firms: Numerous Chinese manufacturers lead the entry-level and industrial polymer segments, while Japanese and Korean companies specialize in advanced metal AM and high-precision solutions.

Competition is intensifying around hardware innovation, specialized materials, automation of post-processing, and integrated production workflows. Service bureaus and contract manufacturers are also expanding as companies seek outsourced expertise.

Challenges

1. Certification & Standards

Industries such as aerospace, defense, and medical require rigorous part validation. Long qualification cycles delay adoption.

2. Material & Process Consistency

Consistency in metal powders, polymer batches, build repeatability, and process monitoring remains a barrier.

3. Post-Processing Bottlenecks

Heat treatment, support removal, machining, and surface finishing often require manual labor, slowing throughput.

4. IP Security & Supply Chain Fragmentation

Design files and production workflows span multiple vendors, raising IP concerns and complicating integration.

5. Skills Gap

Design for additive manufacturing (DfAM) expertise is still limited in many APAC markets, requiring training and workforce development.

Key Opportunities

High-volume Metal Printing

Binder jetting and automated powder-bed fusion will push AM beyond prototyping into true production environments.

On-Demand Spare Parts

Digital inventories and on-site printing reduce logistics cost and downtime, valuable for aerospace, manufacturing, and defense.

Medical Personalization

Custom implants, prosthetics, and medical devices are strong, long-term growth areas.

Localized Manufacturing

AM supports regional production networks, reducing reliance on imported components and unstable global supply chains.

Materials Innovation

Advanced metal alloys, composites, and high-temperature polymers will drive higher-value applications.

Strategic Recommendations

For Technology Providers

Develop integrated solutions that include hardware, software, and post-processing.

Focus on process automation and repeatability for industrial users.

Expand regional support, training, and certification services.

For Manufacturers

Begin with high-value, low-volume parts to establish ROI.

Invest in DfAM training and workflow optimization.

Utilize service bureaus for initial projects to avoid high upfront costs.

For Policymakers

Promote national standards and certification frameworks.

Support AM hubs, incubators, and education programs.

Encourage ecosystem collaboration between industry and academia.

Conclusion

The Asia-Pacific Additive Manufacturing Market is entering a pivotal phase. What once centered around prototyping is rapidly transitioning into production-grade manufacturing across critical industries. With a strong manufacturing base, expanding industrial adoption, rapid technological innovation, and growing regional capabilities, APAC will remain one of the world’s fastest-growing markets for additive manufacturing.